In reference to the recent acquisition of IBM's PC business by Lenovo, as I

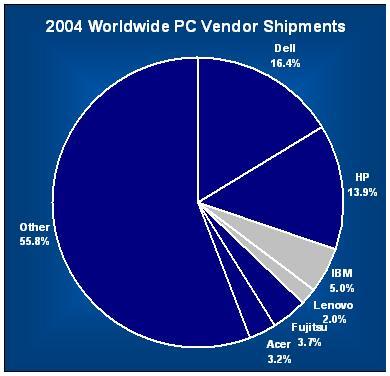

reviewed here, I came across this chart by Gartner Dataquest on the current segmentation of the market:

As noted above, the global market is clearly fragmented with no set market leader. The appears to be lots of room for continued M&A activity and consolidation amongst the smaller players. I bring this up, because I'm rather curious (and somewhat disappointed) with the fact that there were no rumblings of private equity shops bidding on the IBM assets. The fundamentals of the market make it seem like it would have been a timely investment strategy.

Plus, in addition to the roll-up & consolidation opportunities, I still think that there's a lot of growth potential in the market. Now that

thin clients are becoming all the

rage, Internet penetration continues to grow globally, and broadband is becoming more prevalent, I can only imagine an explosion in units sold per average user (not only consumer, but also corporate). Over the longer term, I think Lenovo will have made out on this deal. So it goes.